Problems at Ethos Technologies (LIFE)

Ethos Technologies (NASDAQ: LIFE — $1.26 billion) is on a mission “to protect families by democratizing access to life insurance and empowering agents at scale” through its “leading technology-driven, direct-to-consumer platform.” Ethos is an underwriter, administrator, and distributor of life insurance that helps insurance carriers and agents obtain new policyholders using “advanced digital underwriting, data analytics, and proprietary technology.” Investors believe the company’s capital-light and tech-heavy approach can help transform the fragmented, slow, and outdated life insurance industry.

In reality, The Bear Cave views Ethos as a life insurance lead-generation business. The company spends heavily on TV, radio, and Facebook advertising to drive consumers to its website to request life insurance quotes. The Bear Cave believes Ethos is a mediocre business, has a narrow moat, and, based on records obtained through public records requests, faces allegations of misconduct from consumer complaints filed with regulators.

Founded in 2016, Ethos grew quickly with venture capital backing from Sequoia, Accel, Google Ventures, General Catalyst, and SoftBank. Since its inception, the company has activated over 500,000 insurance policies and now has 600+ employees spread globally from San Francisco to its “engineering and customer success” operations in Bengaluru, India.

Ethos went public in its January 2026 IPO at a $1.3 billion valuation, a roughly 50% valuation haircut from its last July 2021 venture round, a $100 million investment from Softbank at a $2.7 billion valuation.

Last year, the company spent $100 million on advertising to attract consumers to its website. Below are screenshots from some of Ethos’s old TV ads and newer Facebook ads.

On Facebook, Ethos recently started running several ads promoting IULs (Indexed Universal Life insurance) and often publishes videos with the tagline, “Don’t be the dad without life insurance.”

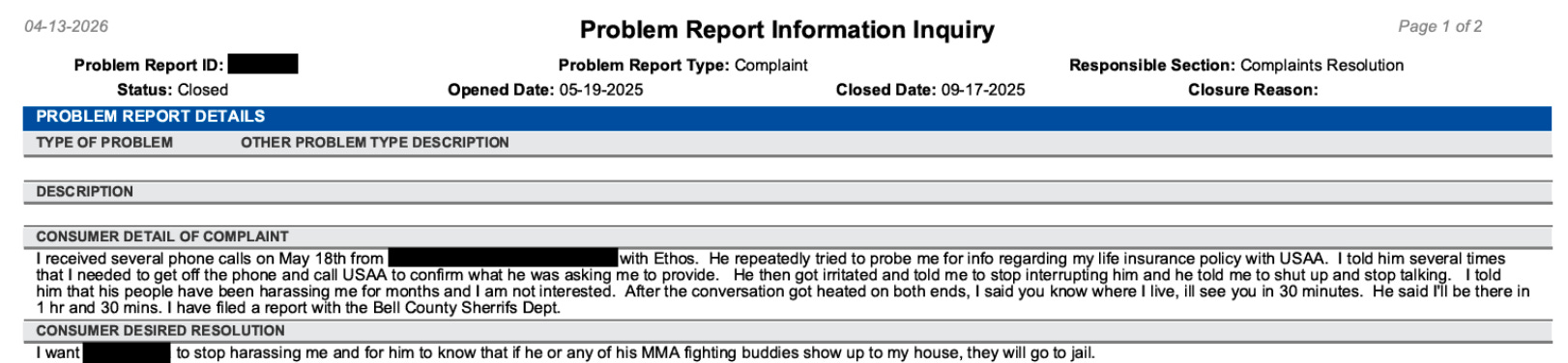

Some consumers haven’t had a great experience with Ethos and the third-party agents on its platform. For example, a May 2025 consumer complaint to the Texas Department of Insurance reads, in part:

“I received several phone calls on May 18th from [Agent] with Ethos… He then got irritated and told me to stop interrupting him and he told me to shut up and stop talking. I told him that his people have been harassing me for months and I am not interested. After the conversation got heated on both ends, I said you know where I live, I’ll see you in 30 minutes. He said I’ll be there in 1 hr and 30 mins. I have filed a report with the Bell County Sheriff’s Dept.”

The consumer added:

“I want [Agent] to stop harassing me and for him to know that if he or any of his MMA fighting buddies show up to my house, they will go to jail.”

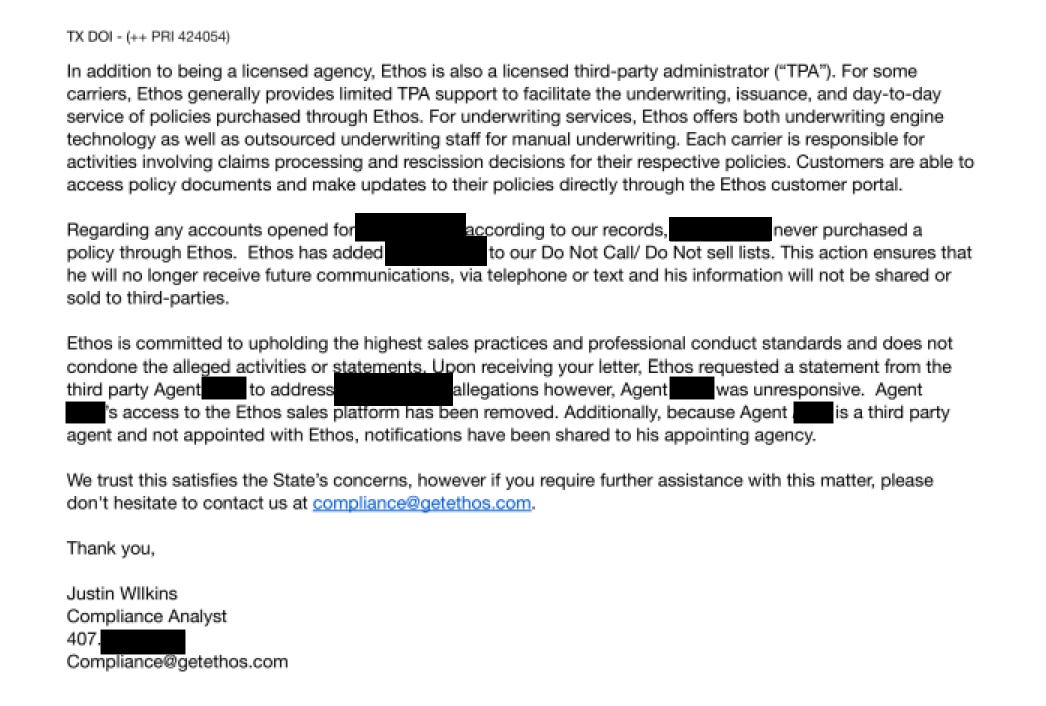

The Texas Department of Insurance forwarded the complaint to Ethos, which responded in August 2025. Ethos noted the customer never purchased a policy through Ethos and added, in part:

“Upon receiving your letter, Ethos requested a statement from the third party [Agent] to address allegations however, [Agent] was unresponsive. [Agent’s] access to the Ethos sales platform has been removed. Additionally, because [Agent] is a third party agent and not appointed with Ethos, notifications have been shared to his appointing agency.”

Other complaints are more serious.