Problems at Kinsale Capital Group (KNSL)

Kinsale Capital Group (NYSE: KNSL — $7.00 billion) is a specialty property-and-casualty insurer focused on “insurance coverages for risks that are unusual or hard to place in the standard insurance market,” known as the excess and surplus lines market.

Kinsale takes on risks that standard/regulated insurers often decline, such as unusual businesses, hazardous operations, companies with poor loss histories, or accounts in difficult legal venues, including bars, contractors, demolition firms, cannabis dispensaries, and jet ski rental companies, among others. Investors believe Kinsale’s industry-leading margins are durable and stem from superior underwriting, proprietary technology, lower expenses, and strong management, all of which have propelled the stock up ~1,560% since its July 2016 IPO.

The Bear Cave believes Kinsale is not a business with a durable moat and instead is powered by overpriced and exclusion-heavy insurance policies enabled by minimal regulatory oversight and a less sophisticated customer base. Through public record requests, The Bear Cave has obtained complaints from Kinsale customers to insurance regulators that allege overcharges and improper billing, as well as insurance so ineffective that one customer claims to have been “defrauded.” The Bear Cave concludes that Kinsale’s business is unsustainable and of low quality.

Founded in 2009, Richmond, Virginia-based Kinsale is led by its founder, Michael P. Kehoe, and has around 700 employees. The company primarily operates on a surplus line basis, which means it is subject to less regulation than admitted carriers and “can generally implement a change in policy form, underwriting guidelines, or rates for a product without being subject to regulatory pre-approval.”

The bear case for Kinsale was best laid out in a July 2025 interview between Brad Safalow and Steve Eisman. In the interview, Mr. Safalow, who runs the independent research firm PAA Research, said in part:

“[Kinsale] is targeting a demographic that is not exactly financially savvy as it relates to insurance… They’re targeting small businesses. Their average premium level is around 14 to $15,000 a year. [It’s] a market that historically people have not targeted…

And so Kinsale has benefited from targeting that market. And from my perspective, they are charging enormous amounts to many of these clients. And they have a 60% retention rate, which for a P&C insurer is extraordinarily low. Most P&C insurers have a 90% retention rate. Now they would argue ‘it’s because we have small businesses and some of them go out of business’ but what I’ve in my own research is that they are charging a lot for a very watered down product because they can…

Ultimately, they’re charging more for less. And what do I mean by less? And this is where it gets into the fine print. I’ve read dozens of their policies. And if you look at the business over the last five years, because it’s been a harder market insurance, they’ve expanded the number of exclusions dramatically… So in effect, in a lot of cases, you don’t really have insurance. And, what we’ve seen is that there’s a lot of litigation against Kinsale because they’re denying claims and they are notorious for not paying.” (41:57)

The Bear Cave encourages readers to watch the full pitch below, starting at 36:06:

Complaints to insurance regulators obtained through public records requests raise similar concerns.

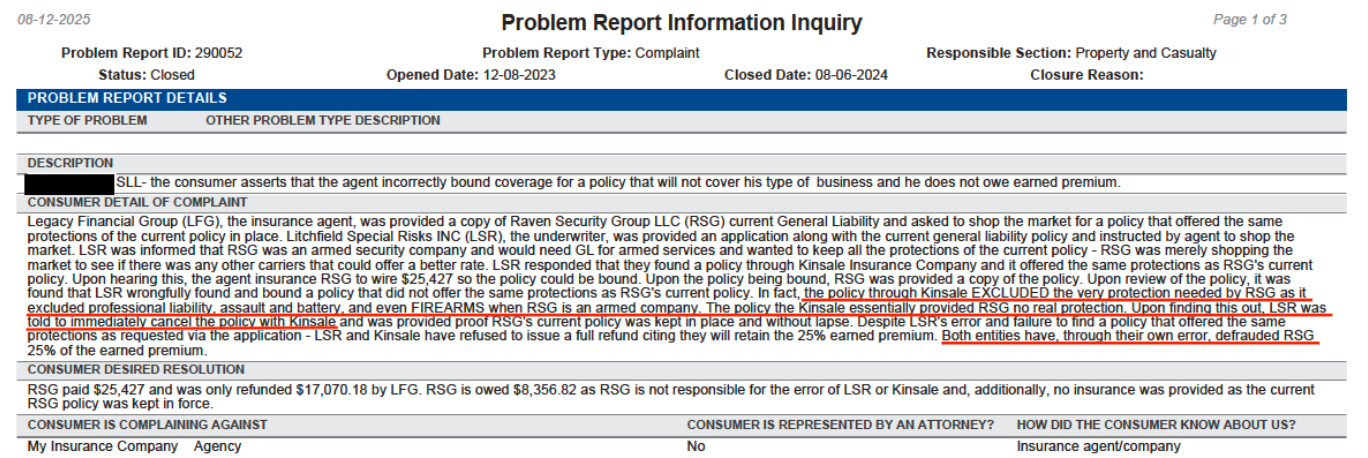

In one December 2023 complaint to the Colorado Division of Insurance, a private armed security company, Raven Security Group (RSG), wrote in part:

“RSG was merely shopping the market to see if there was any other carriers that could offer a better rate. [Insurance broker LSR] responded that they found a policy through Kinsale Insurance and it offered the same protections as RSG’s current policy. Upon hearing this, the agent [instructed] RSG to wire $25,427 so the policy could be bound. Upon the policy being bound, RSG was provided a copy of the policy. Upon review of the policy, it was found that LSR wrongfully found and bound a policy that did not offer the same protections as RSG’s current policy. In fact, the policy through Kinsale EXCLUDED the very protection needed by RSG as it excluded professional liability, assault, and battery, and even FIREARMS when RSG is an armed company.

The [Kinsale policy] essentially provided RSG no real protection. Upon finding this out, LSR was told to immediately cancel the policy with Kinsale and was provided proof RSG’s current policy was kept in place without lapse. Despite LSR’s error and failure to find a policy that offered the same protections as requested via the application – LSR and Kinsale have refused to issue a full refund citing they will retain the 25% earned premium. Both entities have, through their own error, defrauded RSG 25% of the earned premium.”

The complaint was closed in August 2024 after the business filed small claims court litigation against Kinsale.