Problems at Root Insurance (ROOT)

Problems at Root Insurance (ROOT)

The paywall has been removed from our investigation into Root Insurance. If you want investigations like this in your inbox twice a month, please become a paying subscriber of The Bear Cave.

Root Insurance (NASDAQ: ROOT — $3.94 billion) is a car insurance company that is misleading investors and consumers. The company went public in October and claims to use its phone app to distinguish good drivers from bad ones by tracking driving speed, braking, travel times, phone usage, and other factors. Root recently reported improved underwriting results, which it credits to algorithmic enhancements. The Bear Cave believes Root’s results are driven by undisclosed price increases and a one-time pandemic benefit.

In its first-ever conference call on Tuesday Root highlighted Texas, its largest market, as an example of the company’s strong underwriting improvement. In response to an analyst question on its Q3 earnings call, Root’s CFO said:

“Our largest state is Texas... And just look, in Texas, in 2020, we took base rates down. And year-to-date, we've seen loss ratio improvement of about 36 points on 59% earned premium growth. That's quite significant when you look year-over-year at a state which is our #1 state and really shows the benefits of maturity.”

On page twelve of its Q3 investor letter Root doubled down on its improved underwriting narrative. Root wrote, “As you can see in the chart below, the increased predictive power of our telematics and our state management program have driven material direct loss ratio improvements.”

Wall Street analysts trusted management and broadly complimented Root on improved underwriting performance, especially in Texas.

JMP Securities wrote:

“We point to Root’s book in Texas (its largest state) that shows how growth and profitability can work in tandem as markets mature and risk selection evolves (36 point improvementin loss ratio alongside 59% growth in earned premiums YTD 2020, despite taking base rate reductions).”

Barclays wrote:

“Loss ratio also improves after the company has been in a new state with telematics for a year based on new disclosures, which explains why Root will trail the industry averages until all 48 states are up and running”

However, multiple drivers have submitted complaints to the Texas Attorney General about Root Insurance price hikes during the coronavirus pandemic despite no claims, tickets, or other adverse events that may raise prices.

Below are excerpts from the complaints I obtained via FOIA requests.

“…the rate increased 21% even though I have made no claims, have no speeding tickets, and the amount driven … has plummeted due to the pandemic.”

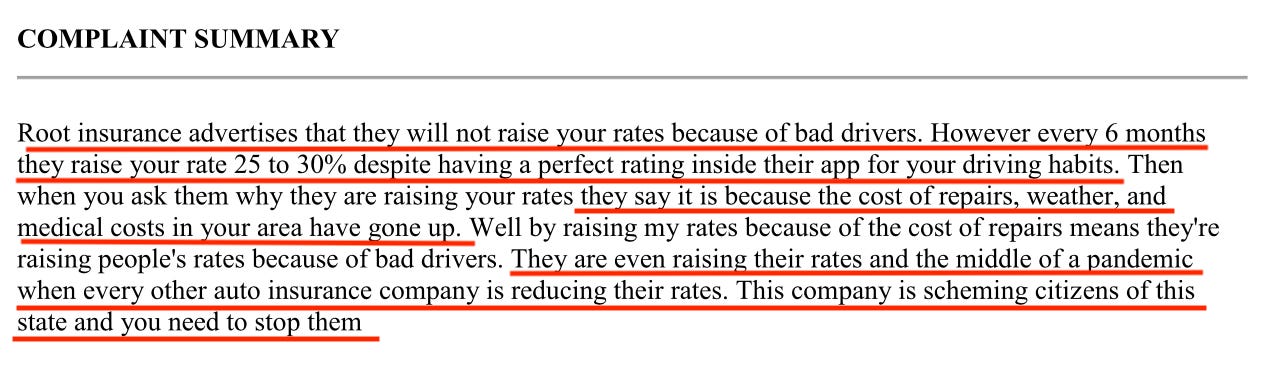

“…they raise your rate 25 to 30% despite having a perfect rating inside their app … they say it is because the cost of repairs, weather, and medical costs in your area have gone up.”

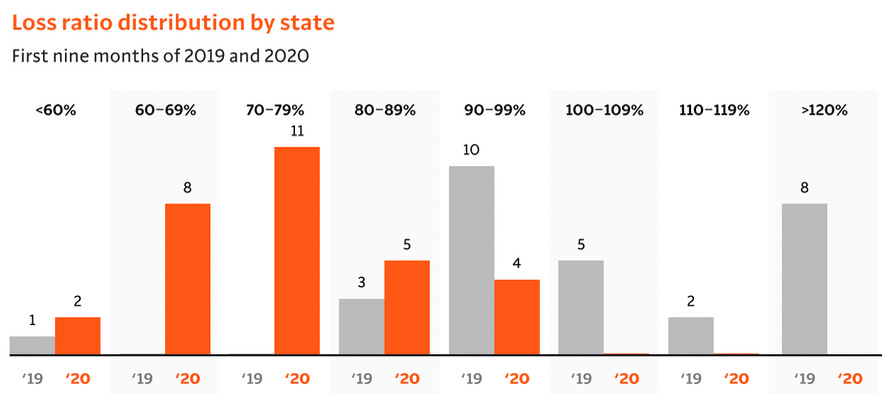

Root is telling investors it lowered base rates in Texas, but consumers are telling the Texas Attorney General they experienced increased rates. Moreover, nearly all other major auto companies, at the prodding of regulators, are rebating customers for the lower driving during the coronavirus epidemic. Unlike Root, other auto companies have shown loss ratio declines of around 20% in addition to sending partial refunds to customers.

Improving loss ratios with price increases is very different than improving loss ratios with price decreases. Price increases are only a temporary solution because they may lead to customer churn.

In Root’s case nearly 2/3 of consumers leave the company after one year, implying Root’s strategy is not sustainable. Most important, Root appears to have directly lied to investors about raising renewal prices.

To find more evidence of potential wrongdoing by Root, I filed a FOIA request for consumer complaints to the Texas Department of Insurance against Root. Because the Texas Department of Insurance had 78 complaints against Root they were not able to supply the documents in time for this article. However, numerous sources across the web detail price increases by Root during the pandemic.

Luring customers with artificially low rates and then bumping them up during a pandemic is not a valuable business model, is not good for building long-term loyalty, and will inevitably attract regulatory scrutiny in the heavily regulated insurance sector.

In fact, Root is currently undergoing “market conduct examinations” in Delaware and Virginia. Below is Root’s disclosure from page 132 of its S-1:

“Root Insurance Company is presently undergoing two insurance department market conduct examinations, one by the Delaware Department of Insurance and the other by the Virginia Department of Insurance. The results of these examinations can give rise to fines and monetary penalties as well as regulatory orders requiring remedial, injunctive or other corrective action.”

The National Association of Insurance Commissioners, a standard-setting and regulatory support organization, publishes data on consumer complaints at auto insurance companies. In 2018, Root had a complaint index score of 1.86, meaning it received 1.86 times as many closed and confirmed complaints as should be expected for a company of its underwriting size (the average score is 1). In 2019, Root’s complaint index score rose to 4.56.

Complaints from other states indicate problems at Root Insurance as well, particularly around policy cancellations. Below is a complaint to the Kentucky Attorney General, where a disabled woman was not given a refund despite multiple attempts to cancel her policy.

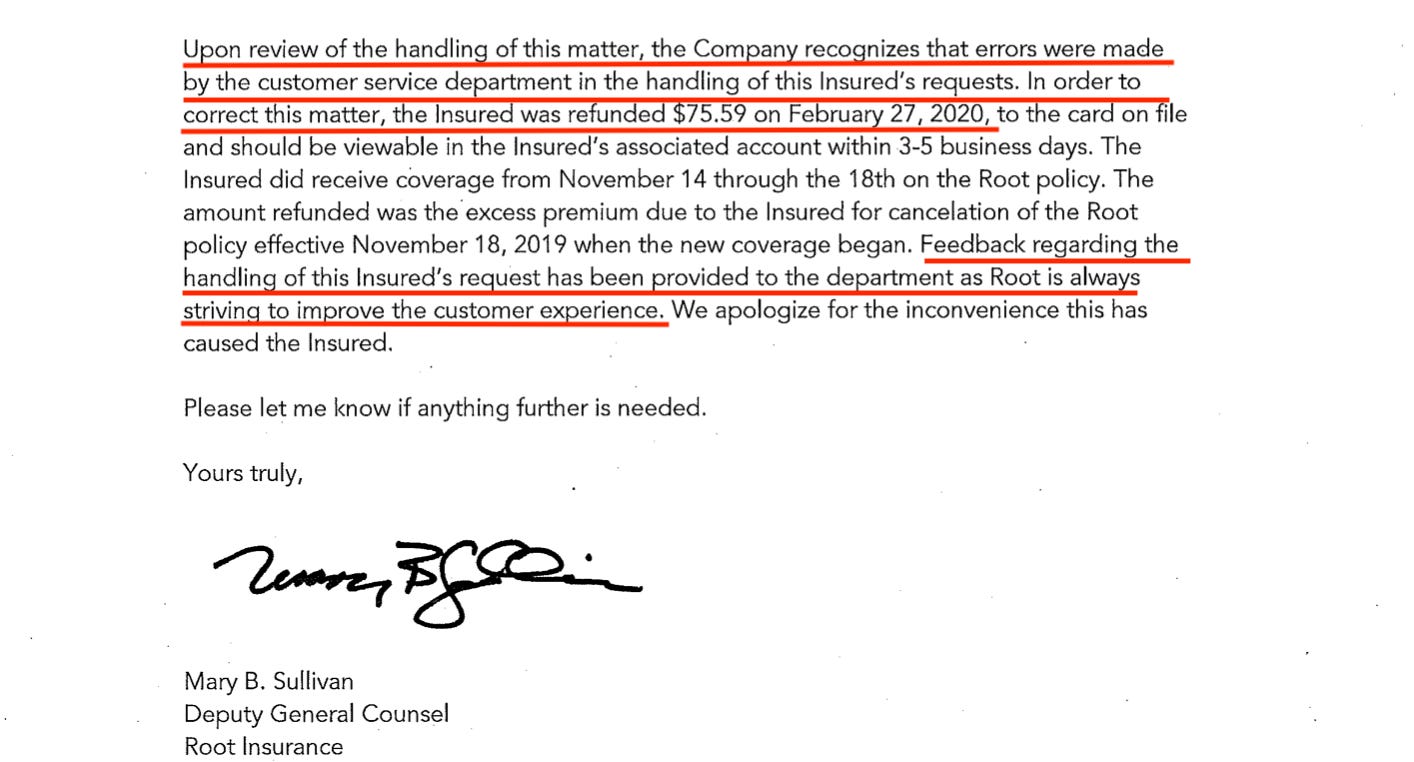

In response, Root’s Deputy General Counsel told the Kentucky Attorney General, “the Company recognizes that errors were made by the customer service department” and “Root is always striving to improve the customer experience.”

According to records obtained via FOIA, the Kentucky Attorney General has also forwarded other complaints to Root for explanation.

In Georgia, another large Root state, a similar pattern emerges. One customer filed a complaint that they needed to call the Georgia Insurance Commissioner’s office to figure out how to cancel their Root policy. Separately, a lawyer representing Spanish speaking citizens wrote the Georgia Insurance Commissioner with concerns about Root’s business practices and suggested potentially revoking its insurance license.

Despite all these problems company trades at a breathtaking valuation. At its current market capitalization Root trades at nearly 6x its premiums in force. An analyst at Citi said it best,

“Typically, an insurance company would be valued on a price-to-book or price-to-earnings basis. We estimate ROOT will have a negative book value and will not generate positive net income in the next few years as it aggressively invests in growth – this creates a challenging valuation dynamic for an insurance company.”

Despite benefitting from lower driving in the pandemic, Root lost $220 million in the first nine months of this year.

Debt markets seem to have caught on to the crazy situation at Root. In November 2019, the company paid LIBOR plus 7% to borrow $100 million in a five-year term loan.

The company currently has about $220 million in cash and $220 million in long-term debt. According to an outstanding report by Insurance Insider, Root is considered to be in distress by some regulators:

“Another indicator of financial distress in its disclosures is that the Ohio Department of Insurance has determined that Root meets the requirements to be monitored under the NAIC’s Hazardous Financial Conditions Standards, requiring the company to file monthly financial reports.”

If Root cannot generate a profit during the best of times — a pandemic which has decreased driving, price hikes, and poor customer service — then how will it ever realize a profit as market conditions revert to normal. Root won’t.

Caveat emptor.

Further Reading

“Root IPO: InsurTech and The Big Lie” (Insurance Insider)

^^ This is an excellent write-up that Insurance Insider has publicly posted on its website.

Q3 Letter to Shareholders (Root IR)

“Metromile: InsurTech & SPAC Dreams” (Substack)

Root Renewal Increases (Twitter)

2018 Podcast with Root’s CEO (Spotify)

This article is not investment advice and represents the opinions of its author, Edwin Dorsey. You can reach the author by email at edwin@585research.com or on Twitter @StockJabber. This article is for paid subscribers of The Bear Cave newsletter. If this article was forwarded to you please consider becoming a paid subscriber to receive articles like this twice every month for $44/month. Learn more here.