Problems at StepStone ($STEP)

The Reckoning Facing The Private Equity Growth Giant

The Bear Cave is thrilled to publish our first investigation in collaboration with Hunterbrook Media’s world-class team of journalists, available today in full exclusively for paid readers of The Bear Cave.

I’m a big fan of this investigation and excited for it to run on The Bear Cave. More investigations from me, and from the Hunterbrook team, ahead.

Disclosure: Based on Hunterbrook Media’s reporting, Hunterbrook Capital is short $STEP and long a basket of comparable securities at the time of publication. Positions may change at any time. This article is not investment advice or a recommendation to buy, sell, or hold any security. See full disclosures below and on Hunterbrook Media's website.

Disclaimer

The Bear Cave newsletter was acquired by Hunterbrook Media in 2026. Please read these important disclosures that apply to all content within The Bear Cave newsletter.

Authors: Bethany McLean, Matthew Termine, JD Jean-Jacques

Editor: Jim Impoco

StepStone (NASDAQ: STEP) is valued at $5 billion on fees it charges for asset management. Those assets have ballooned on paper, driven by stakes in AI companies and SpaceX. But that boom has set up a potential bust. StepStone is obligated to buy out a stake in its retail arm, while the STEP balance sheet only has $200 million in cash. To survive the impending payout, STEP will likely need to raise billions in stock and debt. How did a major global asset manager end up in a liquidity trap?

StepStone helped popularize the “retailization” of private markets — packaging stakes in private companies and private funds into public products sold to retail investors through stockbrokers. The retail arm, StepStone Private Wealth (SPW), grew from about $3 billion in managed assets in 2024 to around $18 billion today.

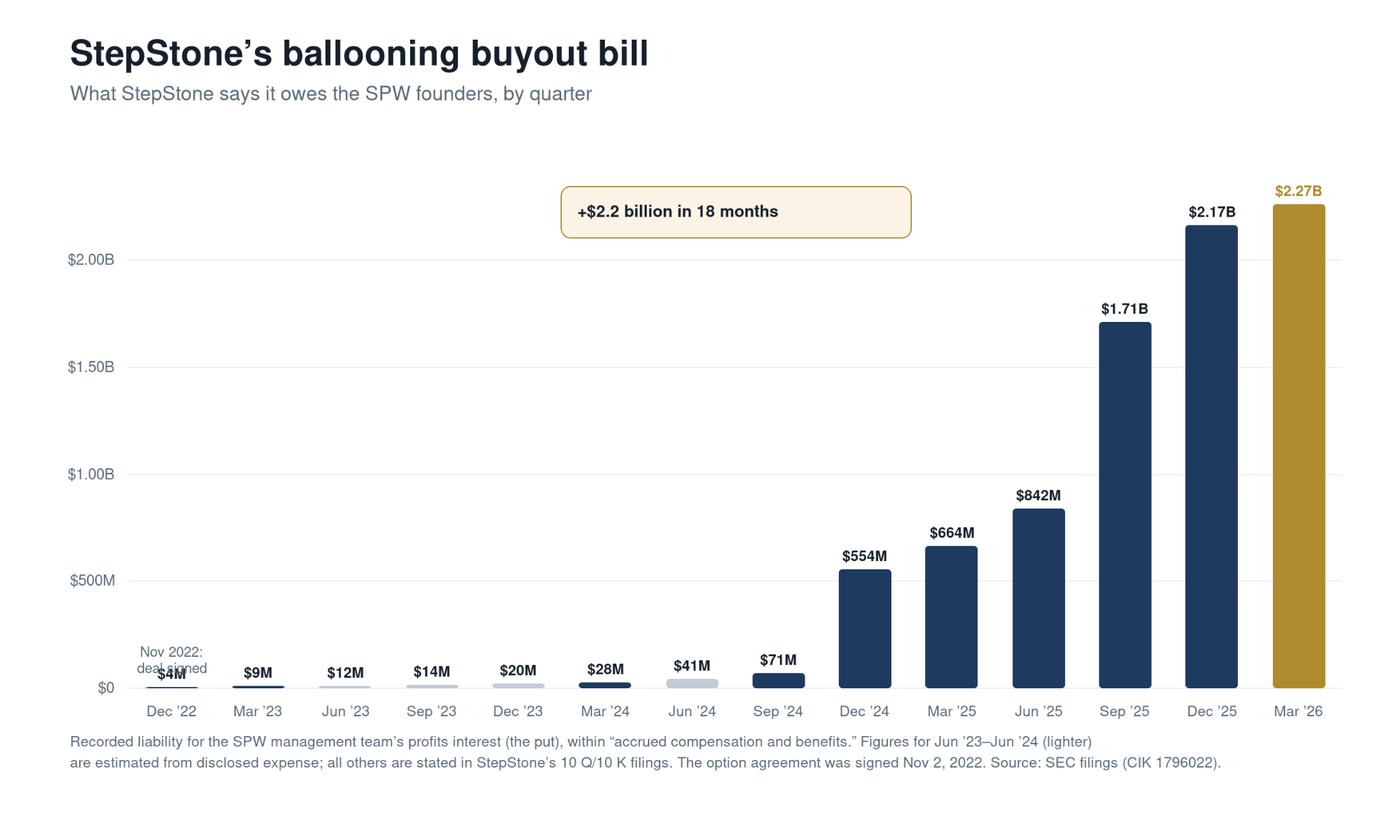

Due to an ill-timed contract, StepStone must buy out the profits interests tied to that retail arm held by CH Equity Partners LLC, an entity controlled by SPW executives. Since April 1, CH Equity Partners LLC has the right to lock in a giant personal payday, using a formula tied to the private wealth arm’s paper marks. StepStone’s liability is now estimated at about $2.3 billion.

How did StepStone end up in this position? The buyout undid an even worse deal StepStone seemingly didn’t disclose at IPO. When the retail arm launched in 2019, CH Equity Partners received an option to buy SPW back from StepStone. StepStone didn’t disclose this contract in its prospectus when it went public in 2020, suggesting the company saw the agreement as immaterial. But SPW soon became core to StepStone’s business — and, in 2022, the company renegotiated its deal, agreeing to the terms of the looming buyout that now threaten to decimate its balance sheet.

StepStone says the buyout could be “accretive,” and, on paper, the deal looks reasonable. Under the hood, the firm must actually pay an extremely rich multiple on recurring fees. We estimate StepStone is paying more than 40 times the trailing recurring fee-related earnings it is actually acquiring. That’s around triple what Stepstone, itself, fetches for its stock in public markets — and a higher valuation than the top firms in the industry, like Blackstone and Apollo. In total, the stake StepStone is buying received $53 million last year in recurring fee-related earnings, less than 3% of what STEP is paying for it. In response to Hunterbrook’s request for comment, StepStone calls this math “fundamentally flawed,” saying it compares a forward-looking purchase price that “accounts for continued growth” against a single year of trailing earnings. The company says the deal is “structured to be executed at a discount to the prevailing STEP multiple.”

The gains underpinning those fees are mostly paper and largely unverifiable. In the key retail fund of SPW, over the last fiscal year, “net unrealized gains for the year were $1.87 billion, while net realized gains were only $3 million,” according to the Wall Street Journal. Over 70% of that fund’s portfolio sits in vehicles whose holdings are opaque, according to Hunterbrook’s analysis, raising questions regarding how ordinary investors can vet these marks. StepStone disputed this framing in its statement to Hunterbrook, saying SPRING’s marks are set under fund valuation policies, reviewed by “reputable external auditors” and “an independent board of trustees,” and that it obtains “positive assurance from a third-party valuation agent on all material positions at least once per year.”

To pay the bill, StepStone seemingly must dilute shareholders, issue debt, or both — with an SPW liability that has already pushed the book value below zero. Management has said the deal will be paid for “largely” in stock, likely devaluing existing shares by about a fifth, with the rest owed in cash it says it may raise in debt. StepStone told Hunterbrook in its statement that it “will be able to meet the cash requirements,” funding the cash portion through “cash on the balance sheet, future operating cash flow, capacity on our revolving credit facility, and flexibility to raise capital.” It also noted: “We remain in continuous dialogue with CH Equity Partners LLC, and we believe that we will be able to meet the cash requirements for settlement of the liability, should they decide to exercise the put option.”

StepStone defended the transaction in a detailed response to Hunterbrook. The company says the buyout is priced at a discount to StepStone’s own trading multiple, that SPRING’s marks are reviewed by external auditors and a third-party valuation agent under an independent board, and that the economics are held by an entity — CH Equity Partners LLC — whose ownership is aligned with the interests of the overall company. On its marks, StepStone has said gains may be “unrealized,” but “that does not make it unreal.”

“The indignation school of writers never tires of pointing out the millions that are stolen in the Street. But while the millions are being stolen, the billions are being lost.”

Stock-broker-turned-author Fred Schwed Jr. wrote that in 1940, a decade after the crash that ended the Roaring 1920s, in his classic: “Where Are the Customers’ Yachts?”

Eighty-six years later, a $5 billion asset manager called StepStone Group ($STEP) has built a machine Schwed would have recognized. It collects real fees off gains that exist only on paper. And it has structured those paper gains so that if they reverse, the paper gains aren’t clawed back. The losses land on everyone else.

One of the cleanest windows into this machine is the recent SpaceX ($SPCX) IPO. StepStone’s flagship retail fund, known as SPRING, paid roughly $270 million for a direct stake in the rocket company. By the end of March, StepStone’s internal valuation committee had marked that same, unchanged stake up to about $587 million — booking a $317 million gain without selling a single share.

SpaceX has become the fund’s largest position at around a fifth of the entire portfolio. The firm charged its retail investors lucrative performance and management fees on that upward paper march, and those fees were paid out to the firm — even though StepStone has not cashed out.

This was, inarguably, a good trade for StepStone!

But now that SpaceX trades publicly, StepStone’s investors are in a bind that Schwed would have recognized instantly: Nearly anyone in the world can now look up what SpaceX is worth and sell it in seconds — except the retail customer who owns it through SPRING.

Because private-market “evergreen” funds are tightly gated, these everyday investors can pull out only a sliver of their money each quarter, and management retains the right to freeze withdrawals entirely if a market panic hits. The fees on the gain have already been spent or allocated away. Some portion of the gain itself can still vanish. And if it does, the captive retail customer takes the absolute loss, while the insiders keep the cash.

That is the micro version of the story — and it’s an example of why existing SPRING investors may now be tempted to leave the fund; and why prospective investors may be harder to convince to join. Why pay 15% performance fees on an illiquid SpaceX investment when $SPCX is trading in the open market?

And to be clear: This is one of the best examples of StepStone’s investments. Most of its portfolio companies have not gone public — and do not have marks that can be verified from the outside.

But there is a bigger story lurking here. StepStone itself faces a massive liquidity crisis. StepStone’s fastest-growing business is its retail arm, StepStone Private Wealth, which bundles private investments into “evergreen” funds like SPRING and sells them to well-off individuals through their stockbrokers. But StepStone itself doesn’t have rights to a large portion of the profits generated by this business.

Years ago, it handed CH Equity Partners LLC, an entity affiliated with executives who run that business, a share of its profits along with, critically, an escape hatch: the right, beginning this year, to force StepStone to buy them out. StepStone hasn’t publicly disclosed a comprehensive list of the individuals behind the entity, but told Hunterbrook it “includes many members of our SPW team.” It is unclear when CH Equity Partners plans to exercise this right.

The catch? The buyout price appears to be dictated by a formula pegged directly to the fees the funds have generated — including the performance fees StepStone charges on its own paper markups. Consequently, every dollar StepStone marks its funds up doesn’t just trigger a fee for its retail investors; it automatically inflates what StepStone owes its own executives. The paper gains, in other words, transform into a real bill.

And because StepStone has marked up its assets so much in recent years, the buyout already stands at an estimated $2.3 billion as of March 31.

StepStone told Hunterbrook the $2.3 billion figure “reflects the current estimated fair value of the future buy-in price under GAAP as determined with the assistance of a third-party valuation specialist.” It also said this calculation was based in part on “SPW’s projected earnings, which reflect an assumed rate of fund performance for each fund.”

To put that $2.3 billion number in perspective, StepStone’s entire corporate balance sheet holds just $213 million in cash. And that price is staggering by the measure that arguably matters most for an asset manager: what it is paying relative to the earnings it’s actually buying.

Businesses are generally valued as a multiple of their profits — loosely, how many years of earnings it would take to make the purchase price back. StepStone’s own stock trades at about 13 times its trailing fee-related earnings (FRE).

The formula dictating this buyout is different. It forces StepStone to buy CH Equity Partners’ stake at what we estimate to be roughly 43 times the recurring fees the stake generated last year — more than triple the price the market puts on StepStone itself. (StepStone called this calculation “fundamentally flawed” — “mismatched periods resulting in an inconsistent multiple” — because the $2.3 billion liability “accounts for continued growth in the private wealth platform.”)

StepStone did not propose an alternative measure for the multiple.

How can a slice of StepStone’s own profits, valued on the same type of revenue stream, have triple the valuation multiple of the business as a whole?

Because, unlike the typical way of valuing asset management income streams, the buyout formula doesn’t price the stake on its steady, recurring fees alone. It also capitalizes on the fund’s past performance fees — the 15% cut StepStone books every time it marks a holding higher — and pays CH Equity Partners a multiple on those, too.

Look at the SpaceX example: StepStone already charged clients tens of millions in performance fees on SpaceX’s paper markup, Hunterbrook estimates. But, according to the terms of the buyout deal, CH Equity Partners is going to be paid a multiple of the fees it has already received on deals like SpaceX in exchange for their profit interest in the fund — even though there is no guarantee, in the future, a similarly lucrative deal will come around.

To pay the full $2.3 billion insider invoice, StepStone will have to dilute its public shareholders by issuing new stock or borrowing heavily from credit markets — maybe both. (The payout is to be a minimum of 25% cash with the remainder in StepStone stock — with the cash and stock, subject to transfer restrictions, owed in short order once the put is exercised.)

What makes the contract even more absurd, at least from StepStone’s perspective, is that the higher it marks its funds between now and the payout, the more cash and stock it will be forced to pay its own executives.

The millions of dollars in gains are being collected by Stepstone executives. The question this story asks is who, in the end, is left holding the losses that may follow.

StepStone’s looming bill has begun to receive some media attention, from the Wall Street Journal, Barron’s, and the blog Mispriced Assets. You should read those excellent articles.

We took a more forensic look.