Problems at TaskUs (TASK)

TaskUs (NASDAQ: TASK — $1.46 billion) describes itself as “a provider of outsourced digital services and next-generation customer experience to the world’s most innovative companies, helping our clients represent, protect and grow their brands.” In reality, TaskUs is a basic business process outsourcer in an incredibly competitive, fragmented, high churn, brutal industry competing for unsexy tasks from both startups and tech giants. Although the company frames itself as an AI winner, The Bear Cave believes TaskUs is a massive AI loser as evidenced by recent revenue declines which we believe will accelerate in the coming quarters.

Founded in 2008 and headquartered in San Antonio, TaskUs employs about 50,000 workers with major operations in the Philippines (~30,000 employees) and India (~10,000 employees) and smaller offices in Mexico, Colombia, and the United States. The company started by offering cheap voicemail transcription services and has since grown into a leading partner for companies like Facebook and DoorDash by doing basic tasks around customer service, fraud prevention, content moderation, and image labeling.

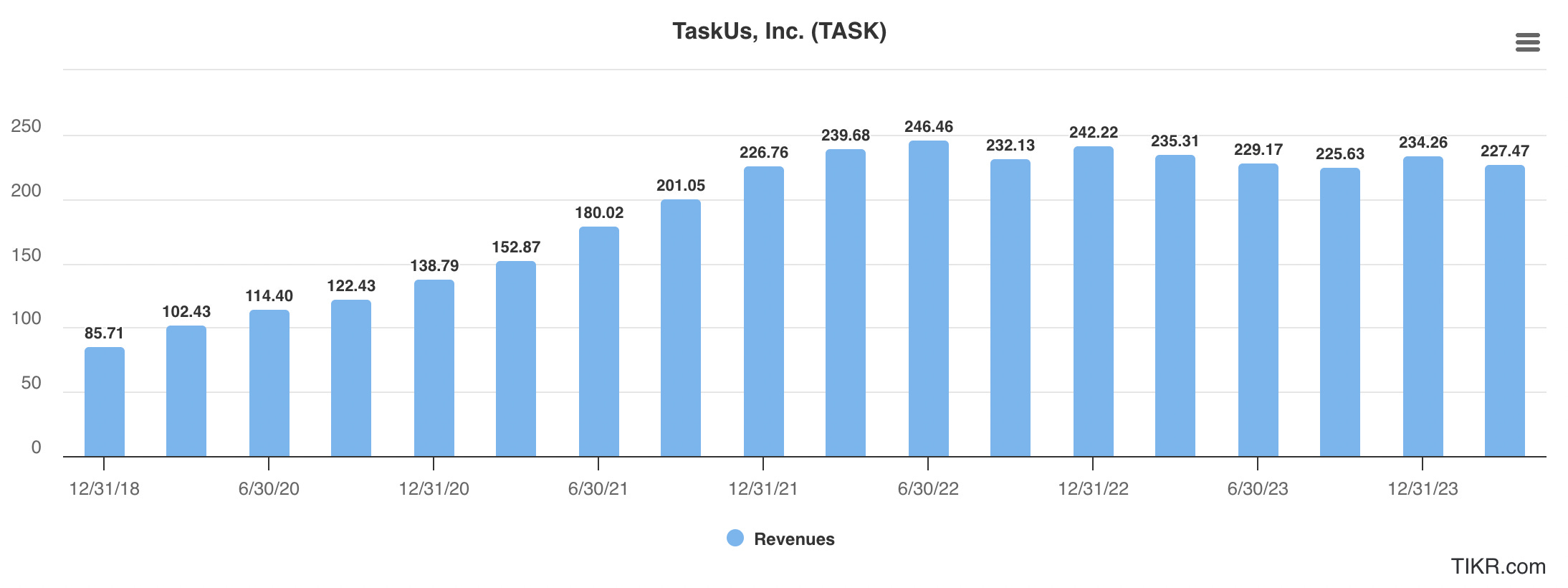

The problem with TaskUs is simple: revenue is shrinking.

In Q2 2022, the company ended its trend of ten consecutive quarters of revenue growth and has now shown persistent revenue declines from $246 million in June 2022 to $227 million in March 2024, a roughly 8% decrease.

The company breaks down revenue into three buckets “Digital Customer Experience,” effectively online customer service, “Trust and Safety,” largely content moderation, and “Artificial Intelligence Services,” mostly labeling datasets to help train AI models.

Aren’t these rapidly growing industries?

The number of online transactions needing customer service is only increasing. And the amount of user-generated content that needs moderation is growing exponentially. And “Artificial Intelligence Services” sounds like it should be taking off in this environment.

Why would a company at the intersection of these fields be shrinking?