The Great Crypto Collapse

The Great Crypto Collapse

Provident Bancorp (PVBC), Silvergate Bank (SI), Customers Bancorp (CUBI), New York Community Bancorp (NYCB), Signature Bank (SBNY), and Metropolitan Bank (MCB)

“After nearly 200 years in the business, we want to be more than just your average bank.”

That is the mission statement of Provident Bancorp (NASDAQ: PVBC — $140 million), which was founded in 1828 and is currently the 10th oldest bank in the country. In 2019, Provident largely rebranded as BankProv “a future-ready commercial bank that is transforming the financial landscape” and began aggressively catering to the cryptocurrency industry.

BankProv “partnered with some of the top digital asset companies,” offered loans against Ether and Bitcoin, provided credit to Bitcoin miners, dabbled in renewable energy projects, worked with a Bitcoin ATM company, and does business with 144 digital asset and fintech clients according to its website.

If you read BankProv’s most recent financials you would assume all is going well. The bank has attracted over $100 million in “digital asset customer deposits” and its “loans to digital asset companies” increased from $15 million on December 31, 2020 to $138.6 million on June 30, 2022. Over that same time period, BankProv’s total allowance for loan losses increased only marginally, from $18.5 million to $18.9 million, an indication its loans were performing well.

Not so fast.

Some signs of trouble with BankProv first emerged in November 2021 when its Chief Lending Officer “retired.” BankProv later disclosed “a $984,000 expense relating to an agreement between the Bank and the President and Chief Lending Officer in connection with his retirement.”

Other cracks quickly emerged. One of BankProv’s largest loans was to Stronghold Digital Mining (NASDAQ: SDIG), an “environmentally friendly” Bitcoin miner. It has fallen ~97% since its October 2021 IPO.

Some of BankProv’s partnerships and integrations also appear dubious. One of its new “strategic integrations” is with Republic, which allows “some of the world's most anticipated crypto projects” to crowdsource funds from investors. Some of the projects soliciting investment on Republic’s platform include “Ember Fund,” a crypto app that charges 3-4% of AUM in fees and “Realm Metaverse Real Estate,” which owns “a diversified portfolio of digital assets across 13 metaverses.”

On Tuesday, BankProv announced that it was unable to file its quarterly results and “indicated that it currently estimates that it will report a net loss of approximately $27.5 million for the quarter.” BankProv also said it “is still evaluating the actual level of losses due to the recent decline in the cryptocurrency mining industry… After $27.4 million loan forgiveness, the digital asset mining loan portfolio totaled $76.5 million at September 30, 2022, of which, upon review, the company estimates a majority to be impaired and placed on non-accrual status with significant related specific reserves.”

Fortunately for BankProv’s digital asset depositors, on its page titled “apply for your crypto business account” BankProv highlights,

“All deposits held at BankProv are fully insured by a combination of the Federal Deposit Insurance Corporation (FDIC) and the Depositors Insurance Fund (DIF). No depositor has ever lost a penny with unlimited deposits backed by DIF.”

BankProv’s CEO, David Mansfield, was previously a bank examiner at the FDIC and a capital markets examiner at the Office of the Comptroller of the Currency. His son, Paul Mansfield, is BankProv’s director of specialty lending.

Despite its dedication to the space, BankProv has nowhere near the largest exposure to the cryptocurrency ecosystem. That distinction belongs to a collection of banks serving the multi-billion “stablecoin” market — cryptocurrencies like USDC, Gemini Cash, and Pax Dollar that are tethered to the U.S. dollar and used as a proxy for cash on many crypto exchanges.

Let’s first look at Pax Dollar, a stablecoin with roughly ~$900 million worth of circulation issued by Paxos Trust Company. Of that $900 million, about $700 million is in Treasury debt and “Treasury Collateralized Reverse Repurchase Agreements” according to Pax Dollar’s unaudited October 2022 holdings report. Another $200 million is held in “insured depository institutions” like Silvergate Bank (NYSE: SI — $992 million) and Signature Bank (NASDAQ: SBNY — $8.68 billion). Paxos’s FDIC Pass Through Insurance Disclosures also lists Metropolitan Bank (NYSE: MCB — $774 million) as a bank that maintains its FDIC-insured omnibus deposits.

Paxos discloses, “Not all deposits are covered by the FDIC or private insurance, and Paxos may still incur losses in the event of a bank insolvency.” Sheila Bair, the former chair of the FDIC from 2006 to 2011 is on the board of Paxos.

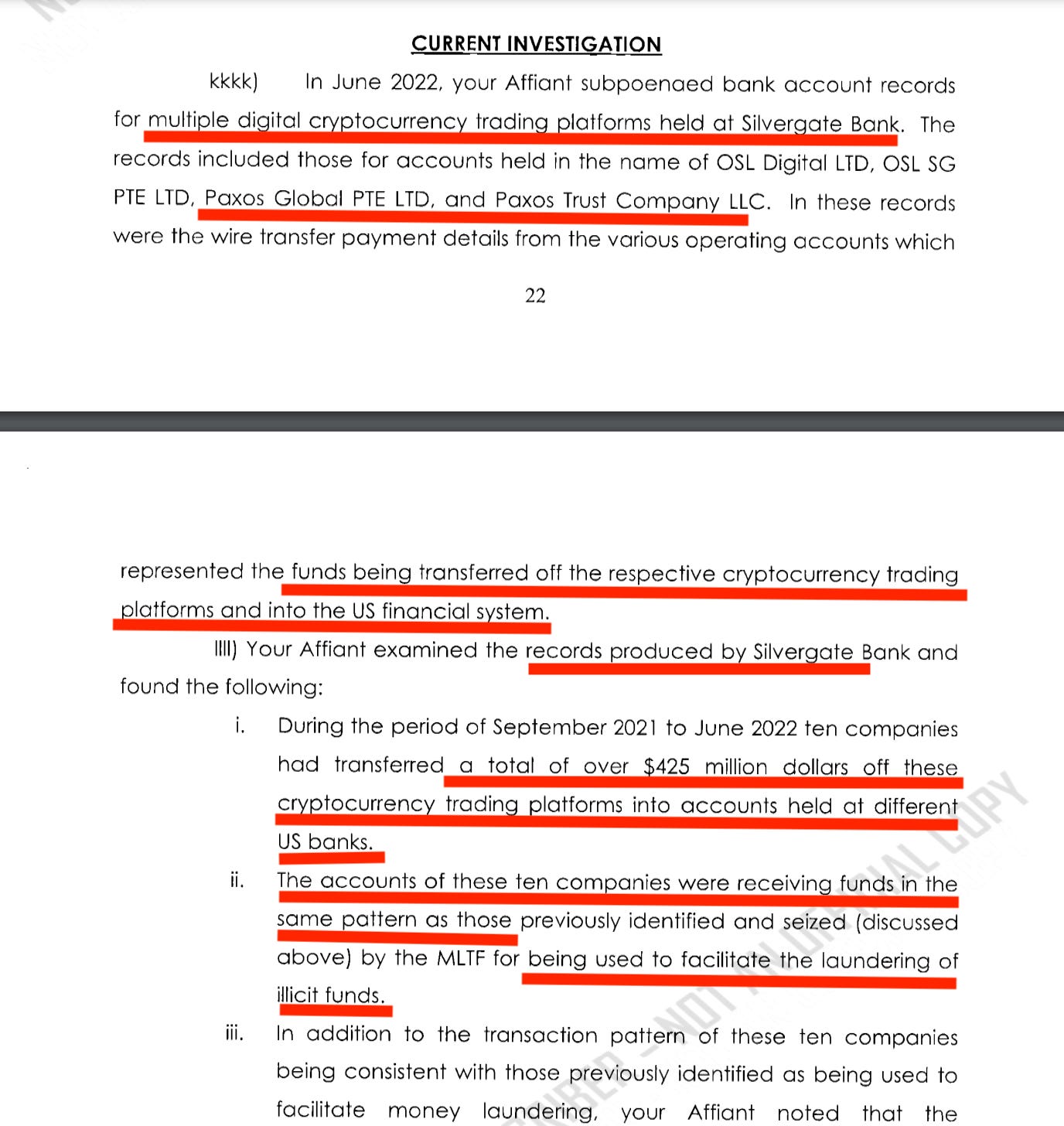

More alarming, an August 2022 forfeiture application for probable cause filed in Broward County alleges Paxos and Silvergate were connected to a money laundering operation. The filing was first highlighted by Marcus Aurelius Research, and it reads in part,

“In June 2022, your Affiant subpoenaed bank account records for multiple digital cryptocurrency trading platforms held at Silvergate Bank. The records for those accounts held in the name of… Paxos Global PTE LTD, and Paxos Trust Company. In these records were the wire transfer payment details from the various operating accounts which represented the funds being transferred off the respective cryptocurrency platforms and into the US financial system.”

The filing continued,

“Records produced by Silvergate Bank found: (i) During the period of September 2021 to June 2022 ten companies had transferred a total of over $425 million dollars off these cryptocurrency trading platforms into accounts held at different US banks. (ii) The accounts were receiving funds in the same pattern as those… used to facilitate the laundering of illicit funds.”

In February 2022, Silvergate, which has ~$13 billion in deposits, boasted that its exchange network “recently crossed $1 trillion in cumulative payment volumes [and] is integral to the everyday operations of our digital currency customers.”

Last week, Silvergate replaced its Chief Risk Officer with its Chief Operating Officer. The former Chief Risk Officer was Tyler Pearson. Mr. Pearson is the son-in-law of Silvergate’s CEO Alan Lane. Silvergate’s Bank Manager of Correspondent Banking is Jason Brenier. Mr. Brenier is also the son-in-law of Silvergate’s CEO Alan Lane. And Silvergate’s Chief Technology Officer, Chris Lane, is the son of Alan Lane. In its most recent proxy filing, Silvergate said the employments were in compliance with its “Anti-Nepotism Policy.”

More concerning is some of the content on Silvergate’s website.

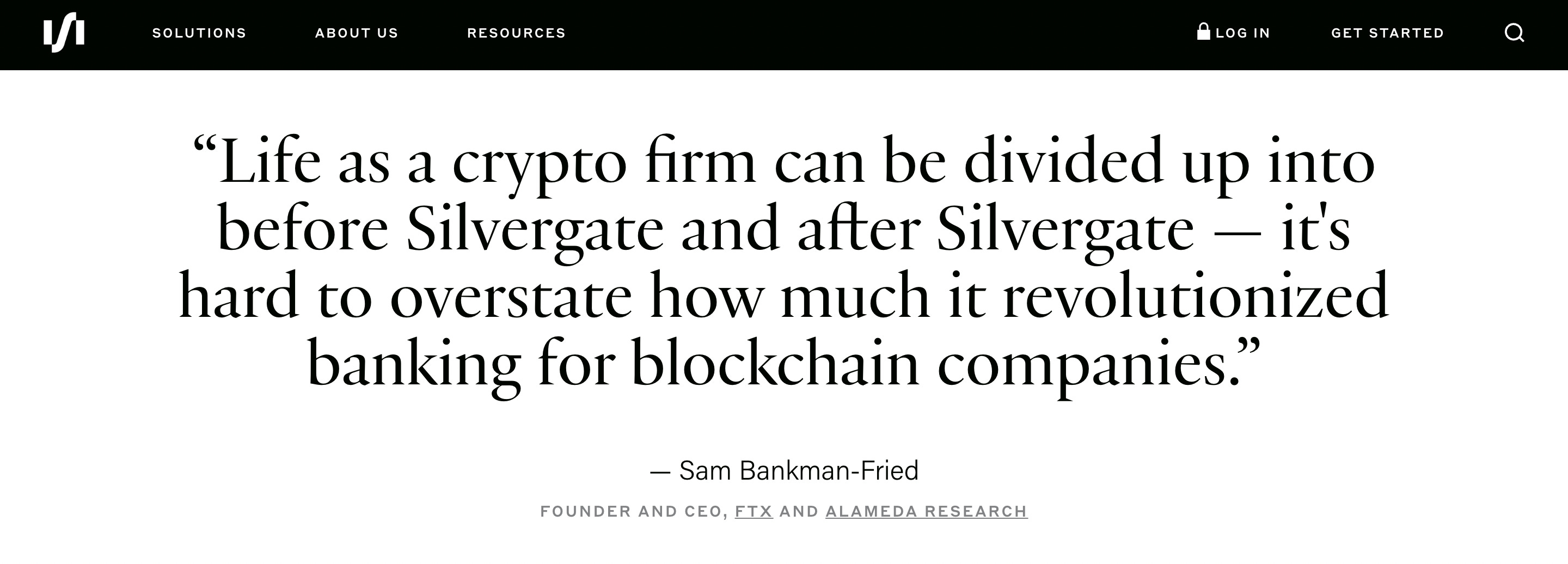

On its homepage until last week, Silvergate had a prominent endorsement from Sam Bankman-Fried who said,

“Life as a crypto firm can be divided up into before Silvergate and after Silvergate — it's hard to overstate how much it revolutionized banking for blockchain companies.”

In a press release after the market closed Friday, Silvergate issued a press release titled “Silvergate Provides Statement on FTX Exposure” and said that as of September 30, FTX represented less than 10% of its total $11.9 billion in digital asset deposits.

Silvergate’s statement ended,

“As a federally regulated banking institution that is well capitalized, we maintain a strong balance sheet with ample liquidity to support our customers’ needs.”

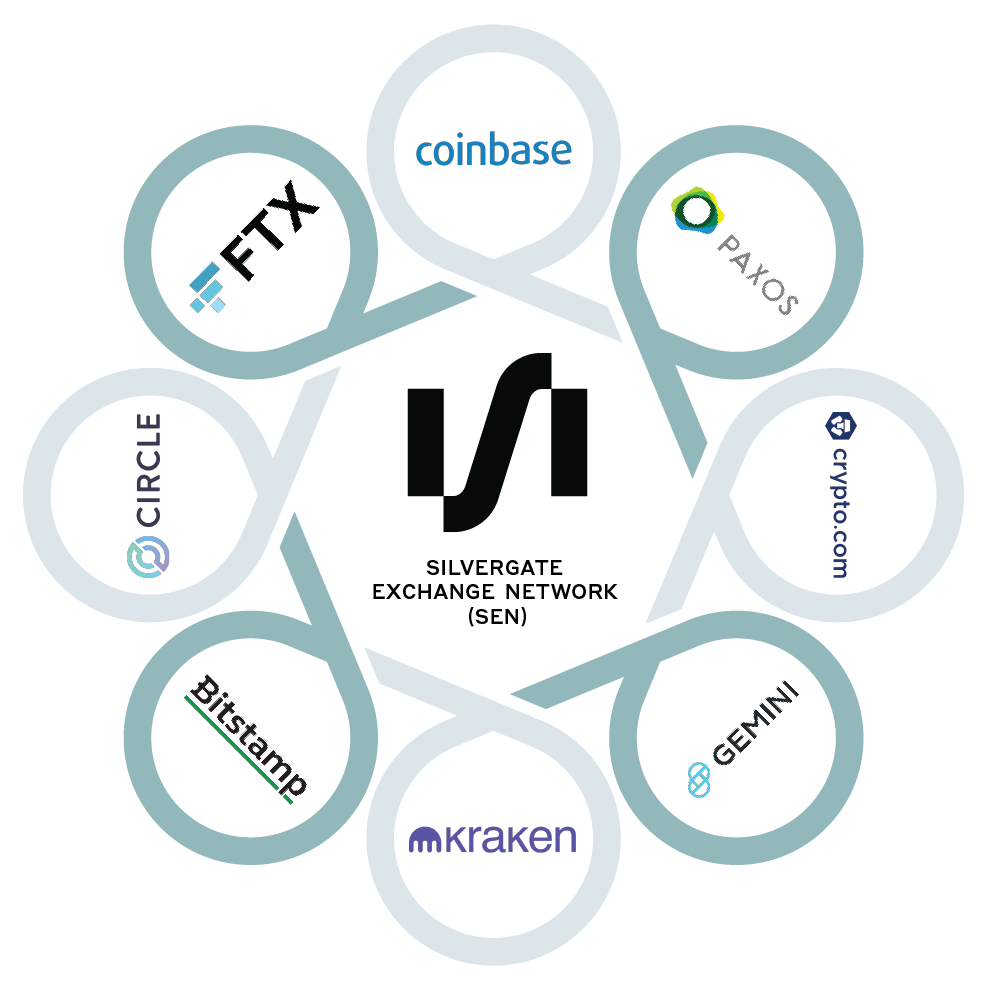

Also on Silvergate’s website was a circular interlocked diagram of its exchange network including the logos for FTX, Paxos, Circle, and Gemini among others.

Gemini, a cryptocurrency platform founded by the Winklevoss twins, also issues a stablecoin called Gemini Dollar that allowed users to earn interest upwards of 7% when enrolled in its “earn” program. Yesterday, that program announced it “has paused withdrawals and will not be able to meet customer redemptions within the service-level agreement of 5 business days” after encountering issues with its lending partner.

The most recent audit attestation for Gemini Dollar, uploaded in Microsoft Word format, shows that the ~$300 million in bank deposits were at Signature Bank, Silvergate Bank, and State Street Bank.

That is dwarfed by the size of USDC, a stablecoin created by Circle Internet Financial. USDC’s outstanding circulation has grown from ~$2.5 billion in September 2020 to ~$47.3 billion in September 2022, the last month Circle published financials.

Coinbase (NASDAQ: COIN — $11.1 billion), which maintains a close relationship with Circle, said on its site in July 2021,

“You can always redeem 1 USD Coin for US$1.00, giving it a stable price. On Coinbase, eligible customers can earn rewards for every USD Coin they hold.”

Coinbase added,

“Each USDC is backed by one US dollar, which is held in a bank account.”

Today that text has been modified to read,

“Each USDC is backed by one dollar or asset with equivalent fair value, which is held in accounts with US regulated financial institutions.”

In its most recent September audit attestation Circle reports having the majority of its assets in treasuries and about $9.2 billion in “cash held at U.S. regulated financial institutions” a figure down from $12.2 billion in July.

Footnote 8 of the auditor attestation says that the banks with Circle’s $9.2 billion in deposits include Customers Bank (NYSE: CUBI — $1.06 billion), New York Community Bank (NYSE: NYCB — $4.51 billion), Signature Bank, and Silvergate Bank, among others.

In a June 2022 podcast interview, Silvergate Bank’s CEO Alan Lane criticized the potential deposit management of banks with billions in stablecoin deposits and said,

“We don't hold all the reserves for USDC for instance. USDC is over 50 billion. We're only a $15 billion bank and we have 1500 customers. So obviously, yeah, we don't have the majority of those dollars. They are spread elsewhere in the banking system. And there are other banks that have, obviously, since we got into the space or other banks that are banking, this, this crypto space, um, and candidly, I think what they're doing with the deposits, and this is not criticism, this is just a factual statement… And so if you were to look at some of the other banks that are banking the space and what are they doing with the deposits, you know, I think they're primarily using those in, in some of their lending operations.” (Emphasis added by The Bear Cave)

For example, Sam Sidhu, CEO of Customers Bank, said in a blog post,

“Crypto businesses have tens of billions of dollars in cash and limited banking options…. For Customers Bank shareholders, banking the crypto industry means the bank can generate tremendous low-cost deposits that fund strong asset growth with a significant net interest margin.”

On a similar note, Signature Bank’s most recent earnings presentation shows that 24% of its $103 billion in deposits come from its digital asset team. In a press release Tuesday Signature Bank said that its “deposit relationship with FTX and their related companies is less than 0.1 percent of the Bank’s overall deposits as of November 14, 2022” (emphasis added by The Bear Cave). FTX also previously highlighted its relationship with Signature Bank for institutional transactions:

More pressingly, what happens if the tens of billions of crypto-ecosystem deposits diminish rapidly?

That is more than a remote possibility, especially given the embedded leverage from crypto lenders like BlockFi that paid 8.6% for deposits of USDC. One finance content creator, Andrei Jikh, who has over 2 million YouTube subscribers, described BlockFi,

“If you are not familiar with BlockFi it is one of my favorite places to keep my crypto online, because they pay me up to 8.6% annual interest compounded monthly, which is crazy. And I know that number is ridiculously high, it sounds like BitConnect or a pyramid scheme, but I promise it’s not. It’s a very legitimate company with very legit investors.”

Yesterday the Wall Street Journal reported BlockFi was preparing for a potential bankruptcy. BlockFi used Silvergate as a “banking partner.”

USDC and its parent company Circle have also come under scrutiny from journalists. Substack author Matt Taibbi published a scathing July 2022 article titled “The Financial Bubble Era Comes Full Circle” and wrote in part, “They’re the mother of all black boxes, and God help anyone invested in them… there was so much spin, the company’s name began to make unpleasantly ironic sense.”

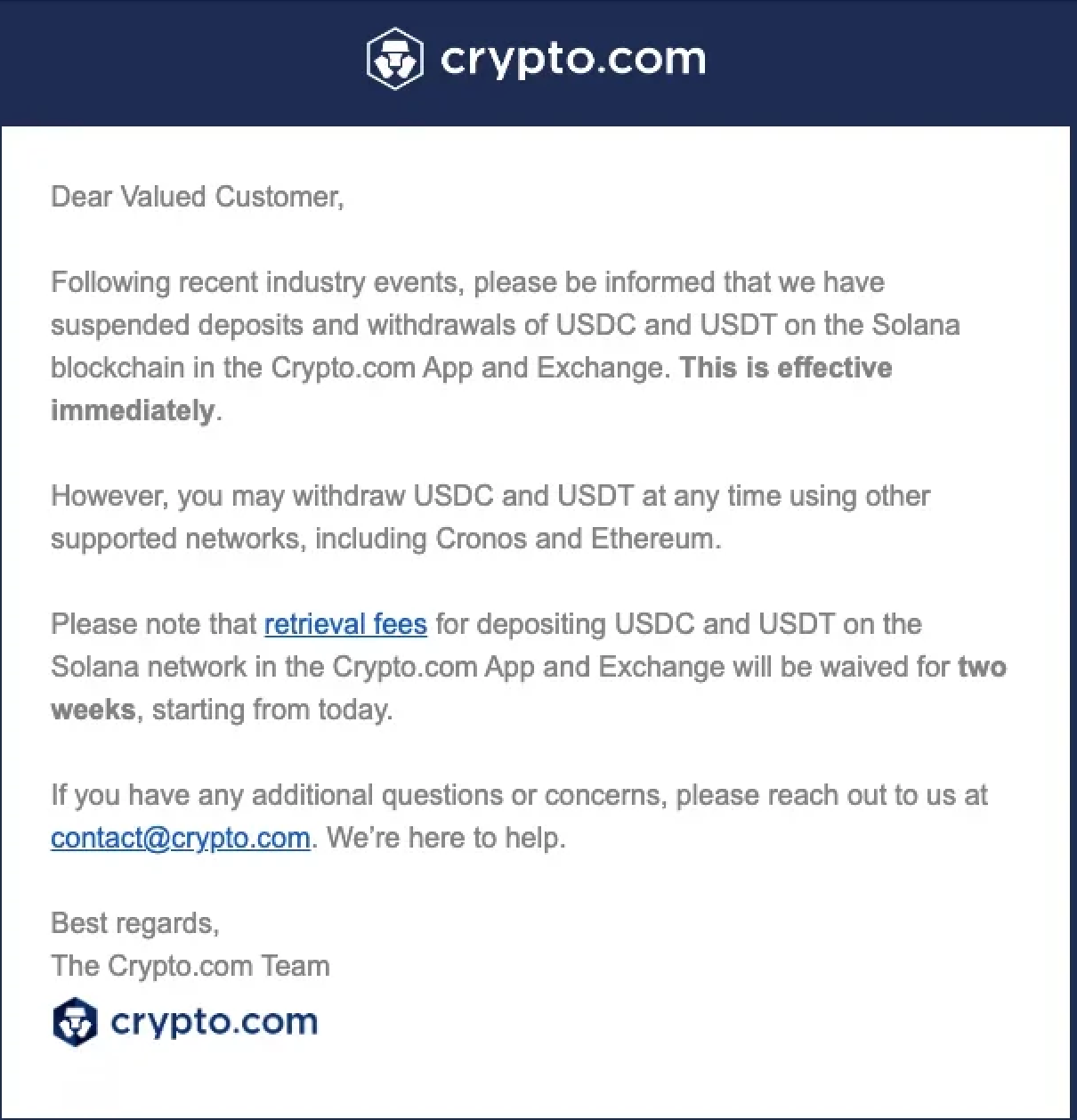

Another sign of problems for the stablecoin ecosystem comes from Singapore-based Crypto.com. According to reporting from Decrypt, on November 9 Crypto.com sent an email to all users suspending deposits and withdrawals of USDC on the Solana Network “effective immediately.”

On Sunday, the Wall Street Journal reported that Crypto.com is facing rising withdrawals after the exchange “mishandled a roughly $400 million transaction.”

Crypto.com also offers an incredibly aggressive tiered credit card selection. Users willing to “stake” $4,000 of Crypto.com’s Cronos token (i.e., purchase the token and hold it in their Crypto.com account for at least six months) would qualify for the indigo and green credit cards that offered 2% cashback and a 4% bonus on staked coins. However, users that staked at least $400,000 worth of its Cronos token would be eligible for the “obsidian card” with 5% cash back, an Airbnb credit, a private jet partnership, and an additional 8% per year on all staked coins.

All of Crypto.com’s credit cards are offered through Metropolitan Bank. The value of its Cronos token has declined ~87% this year.

Perhaps the most aggressive of the crypto platforms is Nexo, which promotes that depositors on its platform can “earn up to 16% on crypto” including 12% interest on deposits of USDC. Nexo serves more than 5 million customers in over 200 jurisdictions, has processed more than $100 billion since its inception, and on September 27 announced it was expanding its presence in the U.S. by acquiring a stake in privately held Summit National Bank.

Summit National Bank’s main physical branch is in Salmon, Idaho, population 3,900, and shares its office space with a local salon.

Nexo’s announcement reads, in part,

“In a transformative deal for the industry, Nexo has acquired a stake in the bank holding company that owns Summit National Bank – a US federally chartered bank regulated by the Office of the Comptroller of the Currency… The deal will allow Nexo to offer its US retail and institutional clients services that include bank accounts, asset-backed loans, card programs, as well as escrow and custodial solutions through Summit National Bank.”

Caveat emptor.

This article is not investment advice and represents the opinions of its author, Edwin Dorsey. You can reach the author by email at edwin@585research.com or on Twitter @StockJabber. This article is for paid subscribers of The Bear Cave newsletter. If this article was forwarded to you please consider becoming a paid subscriber to receive articles like this twice every month. Learn more here.